What Year-End Accruals Are and Why They Matter

Built to Thrive Explainer

Read time: 2-3 minutes

Where this fits: This explainer supports the Tax & Financial Discipline guide path.

Updated on: April 24, 2026

Year-end does not always line up neatly with when money moves through the bank.

Sometimes income has been earned but not yet collected. Sometimes expenses have been incurred but not yet paid. Sometimes money has been received before the work has been done. These timing differences are where accruals become important.

Accruals help the records show the right activity in the right period.

The Core Idea

An accrual records income or expenses based on when they were earned or incurred, not only when cash moved.

- This helps answer a more accurate question: What actually happened in the business during this year?

- That is different from only asking: What went through the bank this year?

Why Accruals Matter

If a business only looks at bank activity, year-end results can be misleading. For example:

- work was completed in December, but the customer paid in January

- a supplier bill relates to December, but was paid in January

- a deposit was received before the work was completed

- insurance or subscriptions were paid in advance

- expenses belong partly to a future period

- invoices are outstanding at year-end

Without accruals, income or expenses may appear in the wrong year.

Common Types of Year-End Accruals

Common year-end timing items include:

- accounts receivable

- accounts payable

- prepaid expenses

- deferred revenue

- accrued expenses

- unpaid bills

- customer deposits

- year-end invoices

The names may sound technical, but the idea is simple: some items need to be adjusted so the year reflects the right business activity.

Corporation Context

Accruals are especially important for corporations because corporate financial statements and T2 filing support usually depend on more complete year-end information.

- The corporation’s income statement should reflect business performance for the year.

- The balance sheet should reflect what the corporation owns and owes at year-end.

Accruals help connect those two views.

How This Connects to the Corporate Workbook

In the corporate workbook, year-end accruals may be used to adjust timing differences that are not fully captured by ordinary bank transactions.

The purpose is not to create complexity. The purpose is to prevent the year-end file from depending only on cash movement. A good accrual section helps identify:

- income earned but not yet received

- bills incurred but not yet paid

- amounts received but not yet earned

- amounts paid that relate to a future period

- items the accountant should review before filing

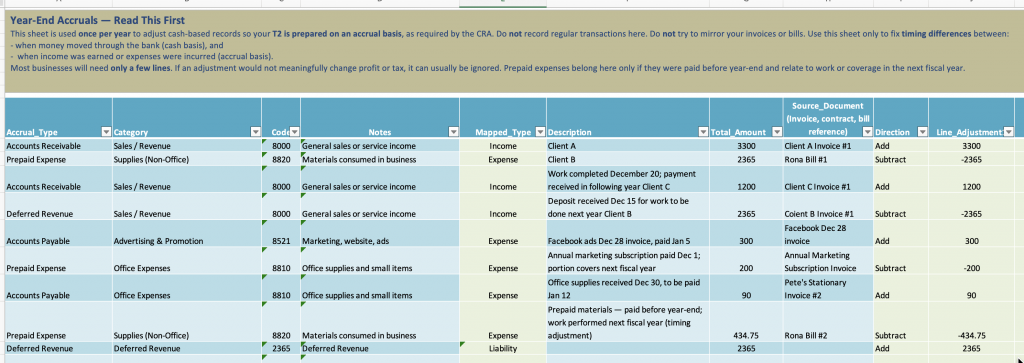

Example Accruals entries:

What to Watch For

Accruals should not be used casually. Do not create an accrual just because an invoice exists. Ask whether the work was actually performed, the expense was actually incurred, or the amount relates to the current year.

- The key question is: Does this item belong to this year, even though the cash moved in another period?

- If yes, it may need review.

What “Good Enough” Looks Like

Your year-end records are stronger when:

- unpaid customer invoices are identified

- unpaid supplier bills are listed

- deposits and deferred amounts are flagged

- prepaid items are separated

- year-end timing differences are not ignored

- accruals have source documents

- uncertain items are marked for accountant review

Educational Note: This explainer is educational only. It is not legal, tax, accounting, payroll, investment, or filing advice. Accrual treatment depends on your accounting method, business structure, source documents, and year-end requirements. Speak with a qualified professional about your situation.