Why GIFI Mapping Matters for a Corporation

Built to Thrive Explainer

Read time: 3 minutes

Where this fits: This explainer supports the Tax & Financial Discipline guide path.

Updated on: April 24, 2026

When a corporation files a T2 return, its financial information needs to be organized in a way that tax software, accountants, and CRA systems can understand. That is where GIFI comes in.

GIFI means General Index of Financial Information. It is the coding system used to organize corporate financial statement information for T2 filing. For an owner-operator, the important point is not to memorize the codes. The important point is to understand that your day-to-day records eventually need to become corporate financial statement categories.

GIFI mapping helps make that transition cleaner.

The basic idea

A corporation’s records need to show more than money coming in and money going out. They need to show what each amount actually represents. For example:

- sales revenue is different from other income

- software is different from office supplies

- subcontractors are different from wages

- equipment may be an asset, not an ordinary expense

- GST/HST payable is a liability, not ordinary business cash

- payroll deductions payable are separate from wage expense

- money owed to the shareholder is different from income or expenses

This matters because the corporation’s year-end file needs to support both an income statement and a balance sheet. The income statement shows performance. The balance sheet shows position.

GIFI mapping helps connect those reports to the categories used in the corporate tax return process.

How this appears in the workbook

In the Small Business Financials Workbook — Corporation, GIFI mapping is built into the workbook as a review structure. The workbook uses practical categories that most small business owners will encounter such as:

| Type | Category | Notes | GIFI |

| Asset | Cash | Bank account balances | 1001 |

| Asset | Due from Shareholder | Shareholder owes Corporation | 1368 |

| Asset | GST/HST Receivable | Refund expected from CRA | 1482 |

| Asset | HST Prepaid | GST/HST recoverable from CRA | 1487 |

| Asset | Accounts Receivable (Trade) | Amounts owed by customers (reporting only if tracked) | 1060 |

| Asset | Inventory | Finished goods or materials held for sale | 1120 |

| Asset | Incorporation Costs | Eligible capital expenditures (Class 14.1) | 2055 |

| Asset | Machinery and equipment (incl. computers/tools/furniture) | Computers, Tools, Furniture | 1740 |

| Asset | Vehicles | Automotive (CCA Class 10 / 10.1) | 1610 |

| Liability | Prepaid Expenses | Prepaid rent, insurance, etc. | 1460 |

| Liability | GST/HST Payable | Net tax owed to CRA | 2310 |

| Liability | Payroll Deductions Payable | CPP, EI, and tax withheld but not remitted | 2590 |

| Liability | Due to Shareholder | Corporation owes shareholder | 2680 |

| Liability | Deferred Revenue | Deferred Revenue | 3400 |

| Liability | Accounts payable and accrued liabilities | Loans, credit cards, etc. | 2620 |

| Equity | Share Capital | Amount paid for shares | 3000 |

| Equity | Common Shares | Common share capital issued | 3240 |

| Equity | Retained Earnings – Current Year | Auto-calculated net income | 3700 |

| Income | Sales / Revenue | General sales or service income | 8000 |

| Income | Professional Service Income | Consulting or professional fees income | 8060 |

| Income | Other Income | Miscellaneous or non-operating income | 8290 |

| Expense | Advertising & Promotion | Marketing, website, ads | 8521 |

| Expense | Professional Fees | Accounting, bookkeeping, legal | 8761 |

| Expense | Office Expenses | Office supplies and small items | 8810 |

| Expense | Software & Subscriptions | SaaS and online tools | 9230 |

| Expense | Meals & Entertainment | 50% deductible client meals | 8523 |

| Expense | Travel | Hotels, flights, taxis (meals excluded) | 8524 |

| Expense | Bank Charges | Monthly fees and transaction charges | 8710 |

| Expense | Rent (Commercial) | Office or commercial space rent | 8911 |

| Expense | Insurance | Business insurance premiums | 8690 |

| Expense | Telephone & Internet | Phone and internet services | 9225 |

| Expense | Supplies (Non-Office) | Materials consumed in business | 8820 |

| Expense | Repairs & Maintenance | Repairs to equipment or property | 8960 |

| Expense | Equipment Rental | Renting machinery or tools | 8915 |

| Expense | Cost of Goods Sold | Costs directly tied to making or selling goods | 8510 |

| Expense | Subcontractors / Contract Labour | Freelancers and assistants | 8230 |

| Expense | Wages & Salaries | Employee wages (salary only) | 9060 |

| Expense | Interest Expense | Business loan interest | 8691 |

| Expense | Bad Debts | Uncollectible invoices | 8590 |

| Expense | Automobile Expense | Vehicle Expenses | 8860 |

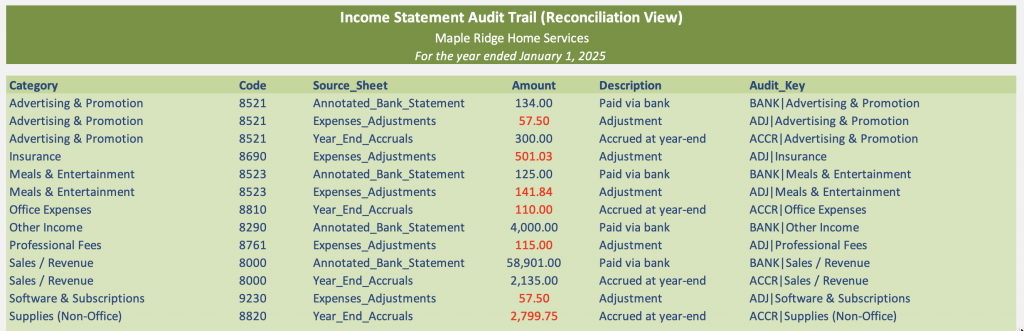

The point is not to turn the owner into a tax preparer. The point is to make the corporation’s records easier to review before hand-off. When entering bank transactions, expenses or year-end accruals, you pick the type from a drop-down which filters the category list drop-down based on the type. the rest of the mappings throughout the reports in the spreadsheet is automatic based on your selections. This Income Statement report illustrates what happens automatically based on your business revenue and expense transactions:

Why the mapping helps

GIFI mapping helps reduce year-end confusion. Without clear categories, the accountant may need to ask basic questions such as:

- Was this business or personal?

- Was this software, office expense, or equipment?

- Was this subcontractor work or payroll?

- Was this GST/HST, income, or a liability?

- Was this money owed to the shareholder?

- Does this belong on the income statement or balance sheet?

Those questions take time because the accountant has to reconstruct what the records should have shown more clearly. Clean mapping does not eliminate professional review. It makes the review easier.

The role of the audit trail

The workbook’s Income Statement Audit Trail supports this process by showing where income and expense numbers came from. It connects reported amounts back to source records such as:

- bank activity

- credit card activity

- expense adjustments

- year-end accruals

- other workbook source sheets

That matters because year-end review should not rely only on final totals. The accountant should be able to trace the numbers back to the records behind them.

If you are not using the workbook

You can still apply the same principle. Use proper categories as shown in the GIFI table above. Keep receipts and invoices. Separate owner transactions. Track GST/HST and payroll amounts clearly. Identify assets, liabilities, shareholder loan amounts, and unresolved items before year-end.

Do not rely only on bank statements. A bank statement shows that money moved. It does not always show what the transaction was, whether GST/HST applied, whether it was business-related, or where it belongs on the corporation’s financial statements.

What “good enough” looks like

Your records are becoming more GIFI-ready when:

- income and expense categories are used consistently

- GST/HST payable is visible

- payroll deductions payable are separated from wages

- shareholder amounts are identifiable

- assets are separated from ordinary expenses

- liabilities are visible at year-end

- income statement totals can be traced to source records

- unresolved items are flagged before accountant handoff

The goal is not to prepare the T2 return yourself. The goal is to keep records that make corporate year-end easier to review, explain, and hand off.

Educational note: This explainer is educational only. It is not legal, tax, accounting, payroll, or filing advice. GIFI mapping, T2 filing, financial statements, shareholder loans, GST/HST, payroll, and year-end adjustments can depend on the corporation’s specific facts. Speak with a qualified professional about your situation.