What Your Accountant Needs for Corporate Year-End

Built to Thrive Explainer

Read time: 3 minutes

Where this fits: This explainer supports the Tax & Financial Discipline guide path.

Updated on: April 24, 2026

Corporate year-end is not just about sending your accountant a bank statement and waiting for a tax return.

A corporation is a separate legal and tax structure. Its year-end file needs to support income, expenses, GST/HST, payroll, owner transactions, assets, liabilities, corporate taxes, and the financial statements used in the T2 process.

The goal is not to do your accountant’s job. The goal is to give them records that are clear enough that year-end becomes a review process instead of a reconstruction exercise.

You can use this explainer whether you are using your own spreadsheet, bookkeeping software, your accountant’s bookkeeping system, or the Small Business Financials Workbook — Corporation.

The system may differ, but the question is the same:

Can someone understand what happened inside the corporation during the year?

The basic idea

Your accountant needs records that explain:

- what the corporation earned

- what the corporation spent

- what the corporation owns

- what the corporation owes

- what moved between the corporation and the owner

- what GST/HST, payroll, or tax amounts need review

- what still needs to be adjusted, explained, or confirmed

Statements and totals are useful, but they are not enough on their own. A bank statement may show that money moved. It does not always explain what was purchased, whether GST/HST applied, whether the transaction was business or personal, or whether it involved the owner.

A good year-end file makes the story easier to follow.

Core records to prepare

Before handoff, prepare the main records that support the corporation’s activity.

That usually includes:

- bank statements

- credit card statements

- loan or financing statements

- sales invoices and customer payment records

- receipts and supplier invoices

- payment processor reports, if applicable

- contracts, leases, and financing documents

- records for major purchases or assets

- GST/HST filings and confirmations, if registered

- payroll records and remittance confirmations, if salary was paid

- dividend resolutions and T5 support, if dividends were paid

- shareholder loan details

- accounts receivable and accounts payable lists

- unresolved questions for accountant review

The point is not to bury your accountant in documents. The point is to make sure the records needed to support the numbers are available and organized.

Owner transactions need special attention

Owner-operator corporations often become messy because money moves between the corporation and the owner without clear labels.

Your accountant needs to know whether owner-related transactions were:

- salary

- dividends

- reimbursements

- shareholder loan advances

- shareholder loan repayments

- personal expenses paid by the corporation

- corporate expenses paid personally by the owner

These are not interchangeable.

Salary needs payroll support. Dividends should be supported by corporate documentation, including a corporate resolution prepared when the dividend is declared or paid. Reimbursements need receipts. Shareholder loan balances need review, especially when amounts owing from the owner remain outstanding around year-end.

Do not leave owner transactions as unexplained transfers.

GST/HST and payroll should be reviewable

If the corporation is registered for GST/HST, prepare support for:

- GST/HST collected

- GST/HST paid on eligible expenses

- input tax credit support

- filing frequency

- filing method

- GST/HST payable or receivable at year-end

- missed, late, amended, or uncertain items

If the corporation uses the Quick Method, or is considering it, flag that clearly.

If salary was paid, payroll should also be organized separately. Payroll is not just an expense category. It may involve gross pay, source deductions, employer contributions, remittances, T4 support, and amounts payable at year-end.

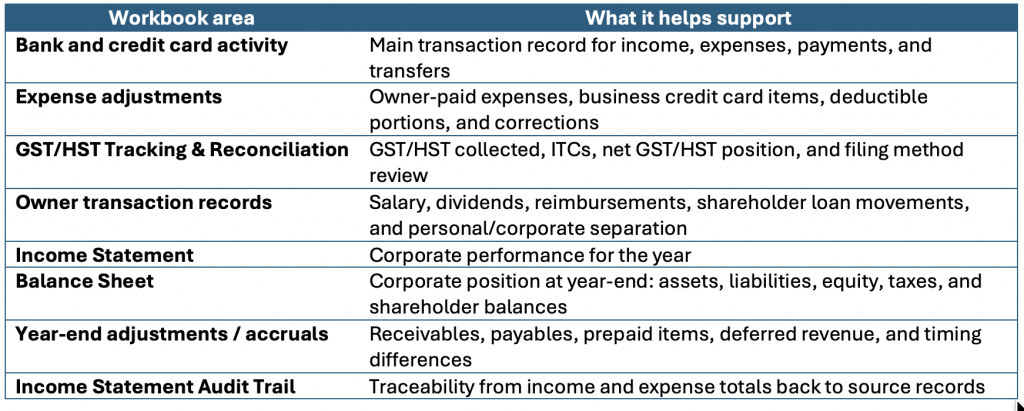

How the corporate workbook supports hand-off

If you are using the Small Business Financials Workbook — Corporation, the accountant hand-off should include both source records and workbook review outputs.

- The Income Statement shows how the corporation performed.

- The Balance Sheet shows what the corporation owns and owes.

- The Income Statement Audit Trail helps explain where the income and expense numbers came from.

That audit trail matters because your accountant should not only see the final total. They should be able to trace the number back to the records that created it.

The workbook does not replace accounting judgment, tax software, CRA filing, or professional review. It helps make the file easier to review, explain, and hand off.

If you are not using the workbook

If you are not using the workbook, the same principles still apply. Prepare a clean package from your own system. That may include exported reports, spreadsheets, statements, folders of receipts, GST/HST summaries, payroll reports, owner-transaction notes, and a list of unresolved questions.

Do not rely on reports alone. Reports are summaries. Your accountant may still need the source records behind them.

Even a simple folder structure, annotated statements, and a short list of open questions can make year-end much easier.

What “good enough” looks like

The corporate year-end file is ready for review when:

- statements are complete

- receipts and invoices are saved

- GST/HST and payroll records are organized

- owner transactions are labelled

- dividends, salary, reimbursements, and shareholder loans are distinguishable

- assets and liabilities are visible

- unresolved items are listed

- income statement and balance sheet reports look reasonable

- source records support the reports or summaries being provided

- workbook outputs are included if the corporate workbook was used

The goal is not perfection. The goal is a file that can be reviewed without rebuilding the year from scratch.

Educational note: This explainer is educational only. It is not legal, tax, accounting, payroll, or filing advice. Corporate year-end, T2 filing, GIFI mapping, GST/HST, payroll, dividends, shareholder loans, and adjustments can depend on the corporation’s specific facts. Speak with a qualified professional about your situation.